Effective budgeting in project management is crucial for ensuring a project’s success. It serves as a financial blueprint, helping managers allocate resources efficiently while keeping expenses under control. A well-structured budget not only outlines the projected costs but also identifies potential financial risks, allowing teams to plan for contingencies. It sets the foundation for financial accountability, guiding decisions that align with the overall project goals.

A comprehensive budget includes various components, such as labor, materials, equipment, and overhead costs. By accurately estimating these elements, project managers can establish a realistic framework that minimizes the risk of cost overruns. It also facilitates better communication between stakeholders, ensuring everyone understands the financial constraints and priorities. This shared understanding fosters collaboration and reduces the likelihood of unexpected challenges during the project lifecycle. Moreover, budgeting provides a benchmark for tracking progress.

Regular financial assessments allow managers to compare actual expenses against the planned budget, enabling timely adjustments and maintaining project alignment. By continuously monitoring financial performance, teams can ensure that resources are utilized effectively and that the project remains on course. Ultimately, budgeting in project management is not just about numbers; it is a strategic process that drives efficiency, transparency, and project success.

Project budgeting is the process of estimating and allocating the financial resources required to complete a project successfully. It involves identifying all potential costs associated with the project, such as labor, materials, equipment, and administrative expenses, to create a detailed financial plan. This plan acts as a roadmap, guiding project managers and teams in managing resources effectively while ensuring that expenditures stay within the approved limits.

A well-defined project budget not only anticipates direct costs but also accounts for potential risks and unforeseen expenses, providing a cushion for unexpected challenges. Beyond financial forecasting, project budgeting serves as a key decision-making tool. It enables project managers to prioritize tasks, allocate resources efficiently, and ensure that every dollar spent contributes to the project's objectives.

A robust budget facilitates transparency and accountability, offering stakeholders a clear understanding of how funds are being utilized. By continuously monitoring and comparing actual expenses with budgeted amounts, teams can identify discrepancies early and take corrective actions. This proactive approach helps maintain financial discipline and increases the likelihood of project success.

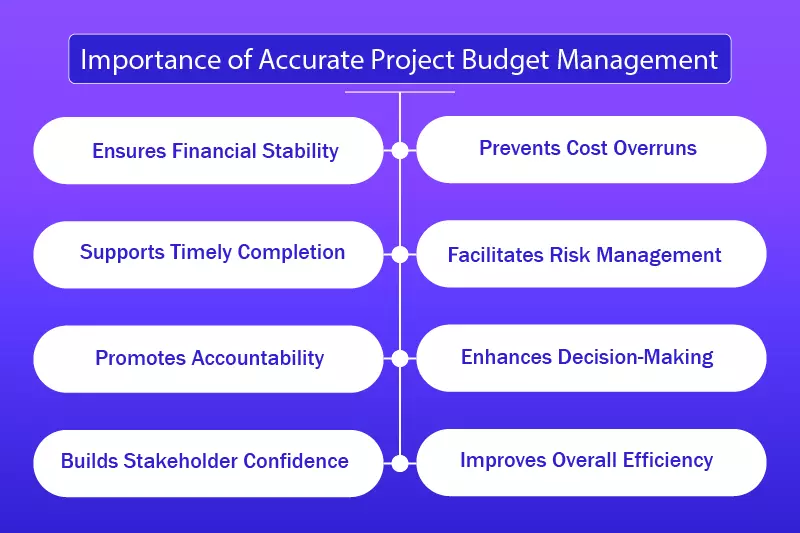

Accurate project budget management is critical to the success of any project, as it ensures that financial resources are effectively allocated and utilized. A well-managed budget helps avoid cost overruns, supports timely project delivery, and promotes stakeholder confidence. It serves as a guiding framework, enabling teams to make informed decisions, address financial risks, and maintain alignment with the project’s objectives.

Without proper budget management, projects are vulnerable to delays, resource wastage, and reduced profitability. By prioritizing accurate budget management, organizations can streamline workflows, improve resource allocation, and minimize financial uncertainties. It not only aids in tracking progress but also ensures accountability across all project phases.

With effective monitoring and adjustments, teams can meet financial goals while maintaining quality standards. This foundational aspect of project management plays a pivotal role in achieving project success and sustaining organizational growth.

Creating budget planning in project management is a structured process that ensures financial resources are effectively allocated to meet project goals. It involves estimating costs, setting financial limits, and monitoring expenses to ensure the project remains financially viable. Budget planning acts as a financial blueprint, guiding teams in decision-making and resource allocation.

By anticipating potential expenses and risks, project managers can proactively address challenges, reducing the chances of cost overruns and delays. Effective budget planning is a collaborative effort that involves input from stakeholders, project teams, and financial experts.

It requires a clear understanding of the project scope, timeline, and objectives. Regular updates and reviews are essential to adjust the budget as the project progresses. With a well-thought-out budget plan, organizations can achieve greater financial control, ensure transparency, and enhance the likelihood of project success.

Effective budgeting is a cornerstone of successful project management, ensuring that resources are allocated wisely to achieve objectives. Budgeting is not just about controlling costs; it’s about planning for every aspect of the project, anticipating risks, and maintaining financial balance throughout the project lifecycle.

A well-crafted budget provides a clear roadmap, enabling teams to operate efficiently and meet deadlines without unnecessary financial strain. Strategic budgeting involves careful planning, continuous monitoring, and collaborative input from stakeholders. By combining accurate estimations with proactive adjustments, organizations can stay on track even when challenges arise.

Adopting proven strategies helps avoid cost overruns, ensures transparency, and builds trust among team members and stakeholders. With the right approach, effective budgeting becomes a tool for optimizing resources, driving project success, and achieving long-term goals.

Project budgeting has become much more efficient and manageable with the advent of various tools and technologies. These tools help streamline the budgeting process, improve accuracy, and provide better financial oversight throughout the project lifecycle.

From simple cost tracking to complex financial analysis, these tools can enhance the project manager’s ability to make informed decisions and stay within budget. Leveraging these technologies allows project managers to allocate resources effectively, track expenses in real-time, and adjust plans as needed. Below are some commonly used tools and technologies for project budgeting:

Project budgeting is a cornerstone of effective project management, offering a multitude of advantages that drive successful outcomes. By providing a clear financial framework, it enables project managers to organize resources, control costs, and monitor progress. A well-crafted budget not only streamlines operations but also minimizes risks and enhances financial predictability.

This ensures projects remain on track, even in the face of challenges, while maintaining alignment with organizational goals. The benefits of project budgeting extend beyond just financial control. It fosters collaboration, boosts team morale, and encourages innovation by creating a structured yet flexible environment.

By aligning financial planning with project objectives, budgeting ensures long-term sustainability and accountability. Ultimately, effective project budgeting acts as a strategic tool that supports seamless execution and optimal resource utilization, ensuring project success.

Project budgets serve as the foundation for monitoring and managing performance throughout the project lifecycle. By defining financial parameters at the outset, they provide a clear framework for tracking progress against planned expenditures. This allows project managers to compare actual costs with the budget, identify variances, and take corrective actions promptly.

A well-structured budget ensures that resources are allocated efficiently, keeping the project on track and aligned with its objectives. It also helps in setting performance benchmarks, enabling teams to measure success and maintain accountability. In addition to tracking, project budgets are essential tools for controlling project performance. They provide the financial discipline needed to prevent overspending and ensure that all activities remain within the defined scope.

With continuous monitoring, budgets highlight areas where adjustments are needed, whether due to scope changes, unforeseen risks, or shifting priorities. This proactive approach minimizes disruptions and maintains project momentum. Ultimately, project budgets act as a guiding force, balancing financial stability with successful execution.

A project budget is essential for ensuring the efficient use of resources and achieving desired outcomes within defined constraints. It provides a structured financial plan that outlines all anticipated costs, helping project managers allocate resources wisely and prioritize critical tasks. By establishing clear financial boundaries, a budget serves as a roadmap, guiding the team through each phase of the project while preventing overspending or resource shortages.

Without a project budget, it becomes challenging to track expenses or maintain alignment with project objectives, increasing the risk of delays and cost overruns. Beyond cost management, a project budget fosters transparency and accountability. It acts as a communication tool, clearly outlining financial expectations for all stakeholders and encouraging collaboration.

Regular budget reviews allow for the identification of inefficiencies and the opportunity to make timely adjustments. This proactive approach minimizes risks, enhances decision-making, and ensures that the project stays on course. In essence, a project budget is not just about managing money; it’s about building a foundation for project success.

A project budget example serves as a practical illustration of how financial resources are allocated, tracked, and controlled throughout the project lifecycle. It provides a detailed breakdown of all anticipated costs, including direct and indirect expenses, and outlines how each expenditure contributes to the project’s overall success. A well-constructed budget not only helps project managers plan but also serves as a tool for monitoring and adjusting financial performance.

By using a project budget example, teams can better understand the cost structure, identify potential financial risks, and ensure that all aspects of the project are adequately funded.

It serves as a reference point for cost estimation, resource allocation, and performance tracking. A clear and comprehensive budget example helps in creating realistic expectations, ensuring that project goals are met while staying within financial constraints.

Project budget management is the process of planning, estimating, allocating, and controlling the financial resources required for a project. It involves defining the total project cost and breaking it down into smaller components, such as labor, materials, equipment, and overheads. This approach ensures that resources are used efficiently and that the project stays within financial constraints.

Effective budget management also includes forecasting future expenses, tracking actual spending, and making adjustments as needed to keep the project on track. It provides a roadmap for financial decision-making and helps in anticipating potential risks. The goal of project budget management is to balance cost control with the need for quality and timely project delivery.

It requires constant monitoring to identify discrepancies between planned and actual spending, as well as the flexibility to make adjustments in response to unexpected changes. Proper management also involves collaborating with stakeholders to ensure alignment and transparency. Ultimately, project budget management supports financial stability, drives performance, and contributes to the overall success of the project.

In project management, both the project budget and project estimate play crucial roles in ensuring a project's financial success, but they serve distinct purposes. A project estimate refers to an approximation of the costs required to complete a project, typically made during the planning phase. It is often based on initial data and assumptions, providing a rough overview of expected costs.

The estimate helps in determining the feasibility of the project and is used to seek approval or secure funding. On the other hand, a project budget is a detailed, formalized financial plan that is developed after the estimate.

It involves a breakdown of all costs, including labor, materials, overheads, and contingencies, and it serves as the baseline for managing and controlling financial performance throughout the project. While an estimate gives a general overview, the budget provides a more refined and accurate representation of the financial resources needed to achieve project goals.

In project management, both the project budget and budget proposal are essential financial tools, but they serve different functions. A project budget is a detailed financial plan created to manage and allocate resources effectively during the project’s execution. It includes a breakdown of estimated costs for labor, materials, equipment, and other project-related expenses.

The budget is developed once the project is approved and the planning phase begins, and it serves as the foundation for monitoring and controlling costs throughout the project lifecycle. In contrast, a budget proposal is a document submitted at the beginning of a project, typically when seeking approval or funding from stakeholders, clients, or investors. It outlines the estimated costs of the project in a high-level overview and presents a case for the project’s financial viability.

The budget proposal is often the first step in securing project approval, and it helps in setting expectations for funding requirements and the overall financial scope of the project.

Accurate project budgeting is crucial to the overall success of a project. Proper financial planning not only ensures that resources are allocated efficiently but also helps in controlling costs, preventing overspending, and ensuring timely project completion. Effective budgeting techniques require diligent planning, real-time tracking, and continuous adjustments as the project progresses.

By following these new strategies, project managers can create a well-defined budget that enhances decision-making and helps avoid unexpected financial risks. A project budget serves as a guide for ensuring that financial resources are utilized optimally.

By using these tips, managers can minimize budget discrepancies, improve forecasting, and drive financial discipline throughout the project lifecycle. Applying these budgeting strategies will help create a stronger foundation for financial planning and execution.

Cost estimation and budgeting are critical elements in project management, as they set the financial foundation for any project. Cost estimation involves predicting the resources and costs required to complete a project, which is done by analyzing available data, historical trends, and expert judgment. This process provides a ballpark figure for expected expenses, helping to define the project's scope and determine its feasibility.

Accurate cost estimation allows project managers to evaluate potential financial risks, plan for contingencies, and secure the necessary funding. Budgeting, on the other hand, takes the estimated costs and refines them into a detailed, itemized plan for managing the project's finances. The project budget includes precise allocations for each cost component, such as labor, materials, equipment, and overheads, with regular updates and adjustments as the project progresses.

The budget serves as a blueprint for managing financial resources and helps ensure that the project stays within financial constraints. By combining effective cost estimation and ongoing budgeting, project managers can control spending, avoid overruns, and deliver projects successfully within the approved budget.

A project manager plays a vital role in ensuring that the project remains within its approved budget. This responsibility is not limited to the initial budget creation but extends throughout the project's lifecycle, with ongoing monitoring, reporting, and adjustment of costs. The project manager is tasked with managing the financial resources of the project while ensuring that the objectives and deliverables are achieved.

Effective budget management is key to a project's success and helps prevent cost overruns and resource shortages. The project manager must collaborate with other stakeholders to gather accurate cost estimates, track expenditures, and make adjustments when necessary. Additionally, the project manager is responsible for assessing financial risks, implementing corrective actions, and ensuring proper financial documentation.

These responsibilities require excellent organizational skills, attention to detail, and strong communication with all team members and stakeholders to ensure that the project stays financially on track.

Project budgeting is a critical process in project management that ensures effective financial planning, allocation, and control. It involves identifying, estimating, and managing the costs required to complete a project successfully.

By understanding and incorporating the basic elements of project budgeting, project managers can better navigate financial risks, allocate resources effectively, and ensure the project stays on track.

Proper budgeting helps ensure that all financial aspects of a project are covered, from resources to unforeseen risks. The essential elements of project budgeting help form the foundation of a well-rounded budget that guides project execution.

Creating a project budget is a crucial part of project management. It serves as a financial blueprint, providing a clear plan for how resources will be allocated throughout the project lifecycle. A well-defined project budget ensures that the project stays within financial constraints, helping prevent cost overruns and delays. It also allows project managers to allocate resources effectively, track progress, and make necessary adjustments as the project progresses.

By breaking the budgeting process into clear, manageable steps, project managers can ensure that all aspects of the project are financially accounted for. These steps not only help in establishing a realistic budget but also ensure that the project is completed within scope, on time, and within the allocated funds.

A well-crafted budget improves project planning and communication among stakeholders and can be a key factor in delivering successful project outcomes. Below are nine essential steps to creating a project budget that can guide your team through this crucial aspect of project planning.

The first step in creating a project budget is defining the project scope and objectives. This helps identify all the tasks, deliverables, and milestones that need financial resources. Clear scope and objectives allow for a better understanding of the specific needs and requirements that form the basis for the budget.

By clearly defining these elements, you can estimate more accurately the resources needed for each phase of the project, reducing the chances of cost overruns. This ensures that every phase of the project is considered and accounted for. The clarity in scope also ensures alignment with stakeholders' expectations. It sets boundaries and helps identify potential risks and uncertainties that could affect the budget.

The next step is identifying the resources and key deliverables required for the project. This includes the workforce, equipment, software, materials, and services needed to complete the project. Accurately identifying resources ensures that all required components are considered in the budget. Without considering the necessary resources, the budget may fail to allocate funds for essential activities, leading to delays and cost overruns.

Mapping out these resources is vital for budgeting accurately. This process also allows you to identify potential gaps or dependencies in the resources needed. Identifying the deliverables ensures that all essential components are budgeted for effectively. By considering the full scope of resources, you reduce the chances of missed or overlooked requirements.

Once the resources and deliverables are identified, estimating the costs for each task or activity is necessary. Cost estimation involves determining how much each component, such as labor, materials, and equipment, will cost. This estimation can be done by reviewing historical data from similar projects, consulting experts, or using standard cost estimation methods. Having a detailed breakdown of costs for every task or activity ensures a more accurate and reliable project budget.

Accurate cost estimates also help prevent underestimation, which can lead to funding shortages. It is important to account for any fluctuations in prices or unforeseen costs in these estimates. Additionally, considering different scenarios and variations in the estimates can help manage potential risks and keep the project within budget.

With cost estimates in place, it’s essential to allocate the identified resources to specific tasks or activities. Resource allocation involves assigning the right people, equipment, or materials to each task based on its requirements and timeline. Proper resource allocation ensures that no task is under-resourced or over-resourced, preventing delays and inefficiencies.

This step optimizes resource usage, helps track resources efficiently, and ensures a balanced distribution of workload across the project. Proper allocation of resources improves team productivity and ensures that resources are used to their maximum potential. It also reduces the possibility of conflicts or resource shortages during project execution. Effective resource allocation allows you to ensure that no phase of the project is neglected and all tasks are completed as scheduled.

Even with a well-planned budget, unexpected events can still occur during project execution. This is why including contingency funds in the budget is essential. Contingency funds act as a buffer for unforeseen costs, such as delays, price increases, or new risks. Typically, contingency funds account for a percentage of the overall budget, depending on the project's complexity and uncertainty.

Allocating contingency funds gives project managers the flexibility to manage risks without compromising the project’s success. The contingency fund should be carefully calculated based on risk assessments and project requirements. A clear plan for when and how to use these funds ensures they are available when needed. Properly managing contingency funds helps keep the project on track financially, even in the face of challenges or unexpected changes.

A detailed project timeline is crucial for determining the budget allocation over time. This includes setting start and end dates for each task, estimating the duration of each phase, and establishing milestones. A timeline helps to track costs throughout the project and ensures that financial resources are available when needed. Additionally, it enables project managers to adjust the budget for delays or early completions, helping maintain control over costs.

A well-defined timeline ensures that resources are allocated effectively and that tasks are completed on schedule. It also helps you evaluate project progress against budget goals regularly. Having a timeline in place also facilitates better communication and collaboration among team members, ensuring that everyone is aligned with project goals.

Labor and material costs typically make up the largest portion of a project budget. It’s important to estimate the total labor cost, including salaries, overtime, and benefits, for each phase of the project. Similarly, material costs should include all supplies and resources required. Accurately estimating labor and material costs ensures that the project budget accurately reflects the true expenses and avoids unanticipated cost increases.

Proper management of these costs is crucial for staying within the financial limits. It’s essential to account for potential fluctuations in labor rates or material prices. Regularly reviewing labor and material costs throughout the project ensures that the budget remains up-to-date and reflects any changes in market conditions. Labor and material costs should be tracked and monitored, especially in longer-term projects where these costs may vary over time.

Once the budget is developed, it’s essential to review and validate it for accuracy and completeness. This review should involve key stakeholders, such as project sponsors, team leads, and financial experts, to ensure that all necessary costs are accounted for and that the budget aligns with project goals. Validation ensures that the project budget reflects realistic estimates and doesn't overlook any costs or resources that could affect the project's financial health.

The review process also helps identify any potential issues or discrepancies in the budget, which can then be corrected before final approval. Validating the budget ensures buy-in from all stakeholders, making sure that the budget is both accurate and feasible. This step helps prevent miscommunication and misunderstandings later in the project lifecycle.

The final step in creating a project budget is to monitor the budget throughout the project lifecycle continuously. Project budgets are dynamic, and adjustments may be needed due to changes in scope, unforeseen expenses, or delays. Regular monitoring and periodic reviews help identify any discrepancies early on, allowing project managers to take corrective actions to keep the project on track financially.

By staying proactive with budget management, project managers ensure that the project remains within budget while delivering expected outcomes. Regular adjustments also allow for resource reallocation when necessary, ensuring that any unexpected shifts in priorities are managed effectively. Monitoring the budget allows you to forecast future spending accurately and adjust for risks or delays promptly.

Project budgeting is a crucial aspect of project management, as it determines how resources and funds will be allocated across different project activities. The effectiveness of a project budget often depends on the method or technique used to estimate costs and allocate resources. There are several budgeting methods, each with its strengths and weaknesses depending on the project's scope, complexity, and requirements.

Understanding these methods and selecting the appropriate one can help project managers control costs, manage risks, and keep the project on track financially. Below are the most common project budgeting methods and techniques used to estimate, allocate, and control costs throughout the project lifecycle.

Top-down budgeting involves determining the total project cost based on high-level estimates from senior management or stakeholders. The budget is then allocated to the different phases or components of the project based on these overarching estimates. This approach typically works well for smaller projects or projects with a clear vision and scope.

However, it may lack the detail needed for larger projects, potentially leading to resource shortages or cost overruns if the high-level estimates are inaccurate. In top-down budgeting, project managers rely heavily on historical data, expert opinions, and intuition to set the initial budget. The process allows for quick decision-making, but the level of granularity may be limited. Once the budget is set, further refinements can be made through more detailed analysis as the project progresses.

Bottom-up budgeting is a more detailed approach where costs for each project task or activity are estimated. These estimates are then aggregated to create the overall project budget. This method provides a higher level of accuracy because it involves input from team members who are familiar with the specifics of the work required. It is particularly useful for complex or large projects where each task's cost needs to be carefully calculated.

While this method provides more granular detail, it can also be time-consuming and resource-intensive. Additionally, bottom-up budgeting can lead to cost inflation if team members overestimate their needs. Despite this, bottom-up budgeting is a preferred method for projects where precise budgeting is critical, as it provides a clearer understanding of cost distribution across different components.

Analogous estimating, also known as top-down estimating, is a technique where historical data from previous similar projects is used to estimate the costs of the current project. This method is quick and less resource-intensive, making it suitable for projects that are similar to others or for early-stage planning when detailed information may not be available.

The accuracy of analogous estimating depends heavily on the similarity between the new and past projects. If there are significant differences, the estimates may not be reliable. This method is often used in the initial phases of project planning to get a rough idea of the budget before more accurate data becomes available. It can also serve as a basis for further refinement once more detailed analysis is conducted.

Parametric estimating involves using statistical data and mathematical formulas to estimate project costs. It requires understanding the relationship between different variables that influence costs, such as time, labor, and materials. For instance, the cost of a specific task might be estimated based on the cost per unit of work or the cost per unit of time.

Parametric estimating provides a more data-driven and precise approach compared to analogous estimating, but it requires reliable historical data and the correct identification of key parameters. This method works well for projects that follow established patterns or processes where historical data can be applied to predict costs. However, it can be challenging if the project involves unique tasks or unfamiliar variables.

Three-point estimating is a technique that uses three estimates to determine a project's cost or duration: the optimistic estimate (best-case scenario), the pessimistic estimate (worst-case scenario), and the most likely estimate (expected outcome). These estimates are then used to calculate an average, often with a weighted factor depending on the likelihood of each outcome.

This method accounts for uncertainty and risk, providing a more realistic estimate than a single-point estimate. It is useful for projects with significant uncertainty or those in the early planning stages. While it provides a broader perspective, it also requires careful consideration of the factors that might lead to optimistic or pessimistic outcomes. The three-point technique can help mitigate risks by accounting for variability in cost and timeline expectations.

Reserve analysis involves setting aside a portion of the project budget to account for unforeseen events or risks. These reserves can be either contingency reserves, which are allocated for identified risks, or management reserves, which are set aside for unexpected challenges that may arise during the project lifecycle. Reserve analysis is an important technique for managing uncertainty and ensuring that there are adequate funds to handle risks without compromising the overall project budget.

The size of the reserve is typically determined based on the complexity of the project, the likelihood of risks occurring, and the potential impact on project objectives. It is crucial for project managers to regularly review and adjust reserve allocations as the project progresses to ensure adequate financial coverage.

Life-cycle costing is a method that takes into account the total cost of ownership over the entire life of the project or product, including maintenance, operation, and disposal costs. This technique is useful when evaluating the long-term financial implications of a project, particularly for infrastructure or large-scale projects that will require ongoing investment.

Life-cycle costing helps identify all hidden costs that might arise after the project is completed, ensuring that the total cost of ownership is considered when making budgeting decisions. It can be especially valuable for projects with long-term objectives or those that involve significant infrastructure development. This method provides a holistic view of costs, helping stakeholders make more informed financial decisions throughout the project lifecycle.

Activity-Based Costing (ABC) is a more refined approach to project budgeting that assigns costs to specific activities within a project based on the resources consumed. It helps identify which activities are driving costs and allows for more accurate cost allocation. ABC is particularly beneficial in projects with complex operations or multiple interdependent tasks.

By analyzing the cost of each activity, project managers can identify areas for cost reduction and optimization. This method also provides a more detailed understanding of cost behavior, enabling managers to make better decisions regarding resource allocation and budget adjustments. However, ABC can be time-consuming and requires detailed data collection to be effective.

Value engineering is a technique that focuses on improving the project's value by assessing its functions and identifying ways to reduce costs without compromising quality. This process involves analyzing project elements to find alternative solutions that provide the same functionality at a lower cost. Value engineering encourages innovation and efficiency, helping to create a more cost-effective project without sacrificing performance or outcomes.

It is often applied during the design or planning phase, but it can also be used throughout the project to identify cost-saving opportunities. The key benefit of value engineering is that it improves the project’s value for money, balancing cost and quality effectively.

Monte Carlo simulation is a statistical method used to predict the probability of different project outcomes based on the variation in key project variables. Running simulations of project costs using random sampling, helps to understand the potential risks and uncertainties that could impact the project’s budget. The technique generates multiple scenarios by factoring in various risk probabilities, which helps project managers assess the likelihood of meeting budget constraints.

Monte Carlo simulations can provide a more accurate forecast than deterministic methods, as they incorporate the inherent uncertainties in project planning. However, the method requires substantial data and computational resources, making it more suitable for complex projects where variability is significant and data is available. Monte Carlo simulation allows project managers to make more informed decisions about contingency plans and budget allocations by highlighting the areas of highest financial risk.

Project budgeting plays a vital role in the success of any project. It helps in the efficient allocation of resources, provides a clear financial roadmap, and enables project managers to monitor expenses, ensuring that the project stays within its financial limits. By using the right budgeting methods and tools, project managers can proactively identify potential risks and adjust plans as necessary.

Accurate budgeting not only ensures that the project is completed within budget but also contributes to maintaining stakeholder confidence and achieving project objectives effectively. Therefore, investing time and effort into detailed and strategic project budgeting is crucial for overall project success.

Copy and paste below code to page Head section

A project budget is a financial plan that outlines the estimated costs of all resources, tasks, and activities involved in a project. It helps project managers allocate funds effectively, track expenses, and ensure the project stays within financial limits. A well-prepared budget is essential for controlling costs and ensuring project success.

Budgeting is crucial in project management because it provides a clear financial framework for the project. It helps control costs, allocate resources, track spending, and identify potential risks early on. A well-maintained budget ensures that a project is completed within financial constraints, reducing the risk of overruns and helping to meet stakeholders’ expectations.

There are several project budgeting methods, including top-down budgeting, bottom-up budgeting, analogous estimating, parametric estimating, and activity-based costing. Each method has its strengths, depending on the project's complexity, size, and available information. Choosing the right method ensures more accurate cost estimates and effective resource allocation.

To create a project budget, project managers first define the project’s scope, identify tasks, and estimate the cost of resources, materials, and labor. The budget is then reviewed and adjusted as needed. Managers also factor in risks and create contingency reserves. Tools and techniques like cost estimation methods can help develop more accurate budgets.

A project budget is a detailed financial plan that includes actual costs, reserves, and contingencies. In contrast, a project estimate is an approximation of the costs and time required to complete the project. Estimates are typically created early in the project, while the budget is refined over time based on more detailed information.

A contingency reserve is a portion of the project budget set aside to cover unexpected costs or risks. It is designed to account for uncertainties that may arise during the project. Contingency reserves help ensure that the project stays within budget, even if unforeseen issues occur.